Excavation Contractors have exposure to different risks than other types of contractors. FarmerBrown.com offers policies to help our customers prepare for any unforeseen outcomes.

Having the right policy in place ultimately helps to reduce loss costs and increase your bottom line. It also keeps jobs running smoothly. Getting the right Excavator Insurance policy is crucial.

As an excavation contractor, you face liability risks each time you begin a job of moving the earth on a construction site. These include risks associated with proper soil compaction, unforeseen sub-surface conditions, and grading for water runoff. You also face exposure to direct damage to your heavy equipment, such as a trench collapse causing equipment to fall into the trench. There are also major risks associated with equipment operator error, hitting underground utilities that can be disastrous.

Further, people or property can be caught in or under heavy materials and equipment causing major damage. Excavators need to grade job sites, dig trenches, run underground piping and cabling and assist in the installation of foundations. This requires the operation of heavy equipment that allows you to move dirt safely and efficiently. Having Heavy Equipment Operators Insurance is necessary for these situations to protect your business from potential claims

We can provide Excavation Contractor Insurance for excavators who perform the following work plus many more:

Excavators are a vital part of many construction sites. Excavation at a job site can lead to many circumstances that can expose you to a considerable risk of loss. The only way to safeguard against huge financial losses in the event of an accident is through effective excavator insurance.

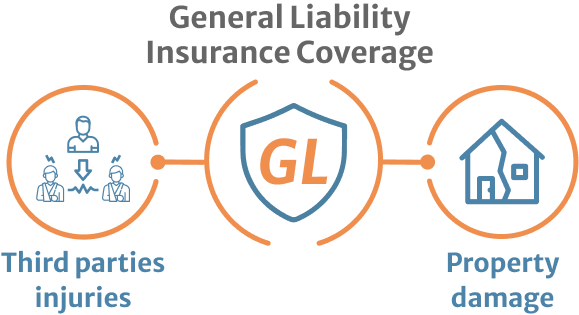

This covers many of the possible situations you face as an Excavation Contractor. It covers property damage and injuries you may cause to third parties while you are doing earthmoving work. Since most of your work is going to come from general contractors they require that you carry at least a certain amount of liability coverage.

Before they let you on the job site they will require you to name them as an additional insured on your policy for the duration of the job. With the many unknown risks faced when excavating a site it would be foolish to operate without the proper General Liability Insurance for Heavy Equipment Operators.

If you hire subcontractors to help you out on a large project, you will want to have them name you as an additional insured on their policies. If you do not when your policy is audited the amount you paid them will not be deductible from your sales. The insurance company will treat them as uninsured subcontractors causing your Excavation Contractors Insurance premium to increase.

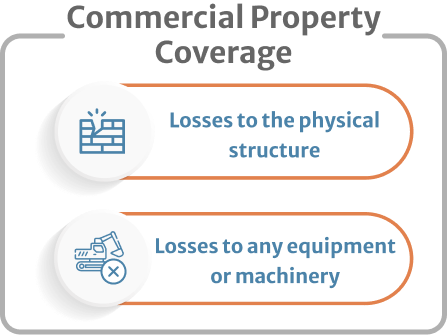

This type of coverage protects the property that your excavating, grading or earth moving business has if you operate out of a physical location. If you have a physical location you should have this coverage. It covers losses to the physical structure and any equipment or machinery stored there.

If a covered loss damages the structure or the machinery/equipment stored inside, your commercial property insurance policy would help to cover the cost of any necessary repairs or replacements. We all know the heavy equipment need to run an Excavation business is expensive. You need to make sure all your equipment has the right coverage. Without your equipment and/or the money to replace it you will be out of business in a hurry.

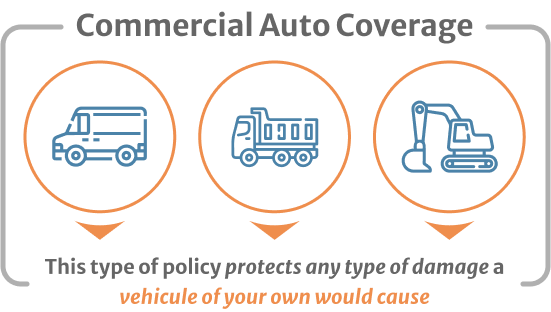

Your personal auto insurance policy will cover any vehicles that are used in your business. This even include your personal vehicle if you are using it for business. If you use trucks, vans, or any other vehicles for your Excavation contracting business, you will need to purchase commercial auto insurance.

This type of policy protects third-party vehicles and other types of property that are damaged as a result of an accident the driver of your commercial vehicles cause. For example, if an employee T-Bones another car while she is driving a work truck, your commercial auto insurance would help to cover the damages of the other vehicle

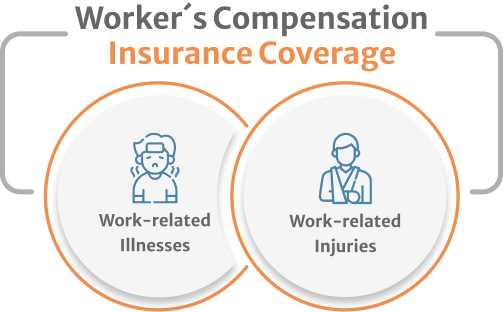

If you have any employees you will also need to carry workers’ compensation insurance. This is the law in almost every State. This type of policy covers and work-related injuries or illnesses that your employees may sustain.

For example, if a during the excavation of a foundation a worker falls into the trench and breaks his leg, workers’ compensation:

Inland marine insurance is coverage that covers your equipment while at the job site or in transit. For example, an Excavator Contractors Insurance inland marine policy will cover theft of skid steers and other equipment from a job site. Because Excavating Contractors and Earth Moving Contractors work off-site, inland marine coverage is essential. Excavating and Earth Moving businesses usually purchase inland marine insurance to cover their expensive and vital equipment.

At FarmerBrown.Com we can handle all your bond needs quickly and hassle-free. There are 2 main situations that Excavation Contractors will need bonds:

Always add the cost of any bond to your original bid, it is an overhead cost like any other. Remember that if the original bid specs did not mention a bond and now the owner is requesting it make sure that they are aware that there will be an additional cost.

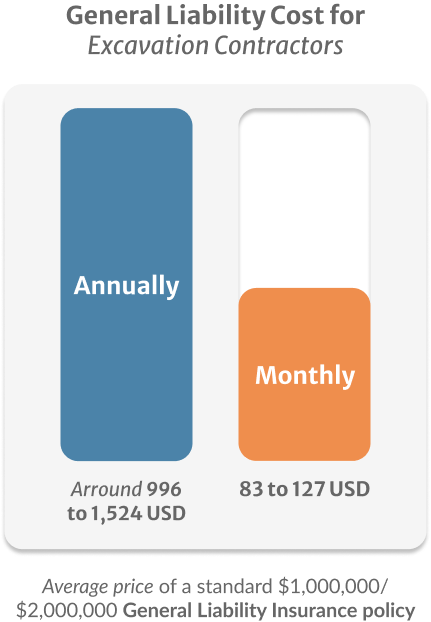

The average price of a standard $1,000,000/$2,000,000 General Liability Insurance policy for small Excavation Contractors Ranges from $83 to $127 per month based on where the business is located, size, payroll, sales, how many years experience and any prior losses. These numbers are just a ballpark quote.

You can contact the experts at FramerBrown.com and they can provide you a firm quote in many cases in less than 15 minutes. The cost of General Liability Insurance for Earth Movers is small considering the protection it provides you and your business.

Our primary goal at FarmerBrown.com is to provide you with the most cost-effective and comprehensive excavation insurance policy possible. We are well aware of the complex challenges faced by contractors seeking to obtain excavator’s insurance to cover their business. Our mission at FarmerBrown.com is to provide you a unique, targeted solution for your contracting business.

We offer a comprehensive range of insurance policies that are specific to the excavation industry. We offer your business a choice from the high costs, poor coverage, and substandard service that is associated with many insurers. Our team consists of industry experts capable of guaranteeing you the most prompt, efficient, and comprehensive service your Excavation Contracting business deserves.

Excavation contractors are routinely required to operate heavy equipment that might be prone to malfunction or be damaged on a construction site.

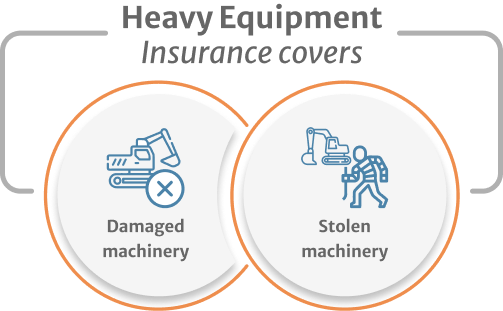

Damage that might result from unexpected operational accidents can cause a significant financial loss to your business; make sure you have the proper coverage. For this reason, Farmer Brown offers additional policies for excavators to insure the usage of and risks involved with heavy equipment. At a minimum, heavy equipment insurance covers the repair and replacement costs for damaged or stolen excavators, cranes, forklifts, bulldozers, and backhoe loaders among other types of machinery.

The machinery required for excavation work is, by nature, prone to damage from malfunction, weather-related events, and user error. Additionally, theft of heavy equipment can occur as the machinery is often left on worksites unsupervised. The cost of repairing this type of machinery is quite expensive, and the replacement costs even more so. By purchasing a heavy equipment insurance policy with sufficient coverage, you are assured years of usage from your machinery and many savings in the event of damages or theft.

Coverage for lent and borrowed equipment varies immensely between policies and insurance providers. If you are lending your own machinery, it is imperative that you confirm third party liability is included in your heavy equipment insurance policy with your provider. It is not uncommon for third-party liability to be outside of a policy’s coverage limits; if you often lend heavy machinery to other contractors purchasing an endorsement package will protect your equipment even if a non-employee is operating a machine during an accident.

If you are borrowing equipment from another contractor, it is equally important to confirm that the contractor who owns the equipment has third party liability coverage with their heavy equipment insurance policy. Additionally, it is necessary to confirm the coverage of borrowed machinery under your own heavy equipment insurance policy if you have one. It is recommended to supply your own policy, even if all equipment used on a site is borrowed, to further protect yourself from paying for damages out of pocket.

Certain excavator insurance policies will cover additional needs concerning heavy equipment. Depending on your coverage needs, we can tailor a policy specifically for your business operations. Some policies will not cover the usage of third party machinery; if your employees prefer to, or are required to, use their own heavy equipment make sure to include employee equipment coverage to your plan.

Additionally, separate coverage may be needed in the event that your machinery breaks down (not caused by user error or damage). Business interruption caused by damaged machinery may be covered under your general liability policy or you excavator insurance policy, however you must confirm this with your insurance provider. If business interruption is not offered under those two policies, it may be provided with a heavy equipment insurance plan. Business interruption coverage is vital for covering labor costs and loss of income if your team cannot operate for an extensive period of time due to equipment malfunction.